Credit card processing fees—often ranging from 1.5% to 3%—can quietly eat away at a company’s profitability. For businesses of all sizes, these costs add up quickly, especially on larger transactions, turning healthy margins into much slimmer returns. According to the merchant advocacy group, the Merchants Payments Coalition, U.S. businesses paid a record $187.2 billion in credit and debit card swipe fees in 2024, an 8.8% increase from 2023’s $172 billion and nearly 70% higher than before the pandemic.

To reduce this expense, many business owners look to surcharge and cash discount programs. Both approaches are designed to shift processing costs away from the business, but they function in different ways and carry unique considerations.

This guide breaks down the advantages and drawbacks of each program, along with the key factors to consider when deciding which approach best suits your business.

Key Takeaways

- Processing fees are costly. U.S. businesses paid $187.2B in swipe fees in 2024, underscoring the need for cost-saving strategies.

- There are two primary strategies to cut card fees. Surcharge and cash discount programs both reduce fees but differ in approach.

- Compliance is essential. Following state laws, card rules, and posting clear signage keeps programs compliant and transparent.

- Customer perception matters. Modest adjustments and clear communication help preserve loyalty while cutting costs.

- RevUpX simplifies fee savings for merchants. RevUpX delivers tailored, compliant solutions that lower fees for margin-sensitive industries.

What Are the Primary Approaches to Managing Processing Fees?

When it comes to managing card processing expenses, most businesses consider two main options: surcharge programs and cash discount programs. Both are designed to reduce processing costs by adjusting how they’re shared with customers.

While they aim for the same outcome, the two approaches differ in execution, compliance requirements, and customer perception. Understanding how each works is the first step toward choosing the program that aligns best with your financial goals and customer experience strategy.

The following sections break down each option:

Surcharge Programs

With a surcharge program, businesses add a small fee to credit card transactions to cover the processing cost.

Example:

If an item costs $100 and the surcharge is 3%, a customer paying by credit card would be charged $103.

Pros:

- Eliminates or reduces credit card processing costs.

- Transparent to customers who use cards.

- Generally straightforward to implement.

- Preserves payment flexibility for customers.

- It can offer an edge over competitors that don’t use surcharge programs.

Cons:

- Surcharge programs are prohibited in certain states (e.g., Connecticut and Massachusetts).

- Cannot be applied to debit card transactions.

Cash Discount Programs

In a cash discount model, prices are displayed at the card price, but customers who pay with cash receive a discount.

Example:

An item is priced at $103 (credit card price). This is the price applied when a customer pays with a credit card. However, a cash-paying customer is offered a reduced price of $100.

Pros:

- This can be applied across all payment types, including debit cards.

- Cash discount programs are legal in all 50 states.

- Cash discounting preserves payment flexibility for customers.

- They can offer an edge over competitors that don’t use cash discount programs.

Cons:

- May require repricing or re-tagging merchandise.

Surcharge vs. Cash Discount: What Customers Pay

*At the discretion of the merchant.

Implementation Considerations

Choosing between a surcharge and a cash discount program is only part of the equation. Successful execution requires attention to compliance, communication, and customer experience:

Compliance

Each program comes with its own set of rules and guidelines. Surcharging has more restrictions and is limited in certain situations, while cash discounting is broadly permitted but must be structured correctly. In both cases, businesses need to make sure they’re aligned with card brand standards and state regulations to avoid issues down the line.

Signage & Disclosure

Customers need clear notice before paying. Post signage at entrances, points of sale, and online checkout. Receipts should clearly show either the surcharge or the discounted price.

Technology

Not all systems handle these programs accurately. Use processors and terminals that automatically apply surcharges or discounts and itemize them on receipts.

Staff Training

Employees should be able to explain how the program works, emphasize customer choice, and reassure customers that the program complies with regulations.

Customer Perception

The success of either program depends on how it’s received. Keep adjustments modest, frame them as a way to offset rising fees, and be transparent so customers feel they’re being treated fairly.

Ongoing Monitoring

Check regularly for updates in state laws and card brand rules. Audit signage and receipts, and measure whether the program is lowering costs without negatively affecting sales.

RevUpX supports a wide range of industries with tailored surcharge and cash discount solutions.

Explore how it works in your field:

- Auto Dealerships

- Home Heating Oil Providers

- Moving & Storage Companies

- Waste Management Services

- Any Business on the Move

Not sure which category fits your business? Talk to our team →

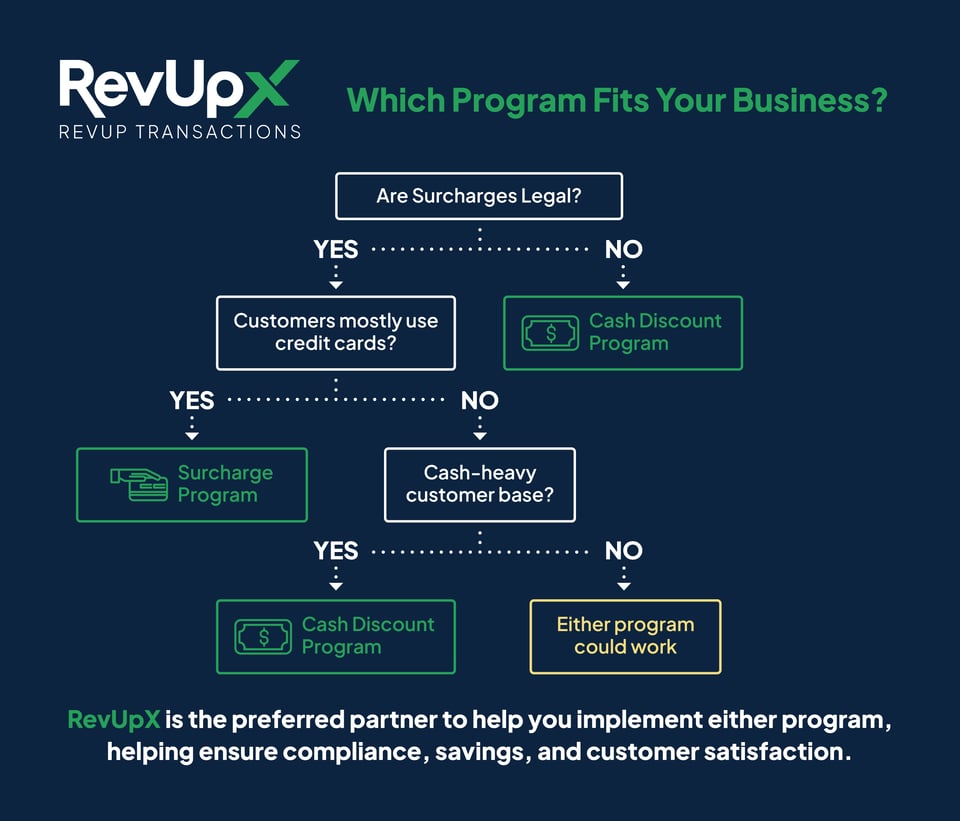

Choosing the Right Program for Your Business

Deciding between a surcharge and cash discount program isn’t one-size-fits-all. The right choice depends on your business model, customer base, and long-term goals.

Before making a decision, consider the following factors:

- Legal Restrictions: Businesses in states where surcharges are prohibited will need to focus on cash discounting.

- Financial Impact: Estimate savings based on your sales mix and the payment methods your customers prefer.

- Pricing Strategy: Consider whether raising listed prices (cash discount model) could affect your competitive positioning.

- Customer Expectations: If your customers primarily use credit cards, surcharging may make more sense. If you have a cash-heavy customer base, cash discounts could be better received.

- Brand & Experience: Weigh how each program aligns with your brand’s approach to customer service.

- Operational Simplicity: Evaluate which program is easier to integrate into your existing systems and staff training.

Partnering With the Right Provider

Regardless of the program you choose, success depends on proper implementation and compliance. Partnering with an experienced payment processor ensures your business avoids pitfalls, maintains customer trust, and captures the full financial benefit.

The right partner can help with:

- Customized solutions tailored to your business model.

- Compliance guidance for state and card-brand regulations.

- Implementation support, including signage, disclosures, and staff training.

- Access to modern payment technology at little or no upfront cost.

RevUpX brings extensive expertise in implementing both surcharge and cash discount programs across diverse industries. With established partnerships with industry leaders such as Fiserv and CardConnect, RevUpX provides the specialized knowledge and technology needed for successful program execution.

The RevUpX team ensures full compliance with regulations while delivering comprehensive implementation support, from initial setup through ongoing staff training and system monitoring, helping businesses maximize their cost savings while maintaining exceptional customer service.

Bringing It All Together

Whether you choose a surcharge or cash discount program, both offer a pathway to significant savings on credit card processing costs. By evaluating your customer base, sales mix, and operational needs, you can implement a program that protects your margins, supports customer satisfaction, and strengthens your bottom line.

Contact RevUpX today to learn how our team can help you implement a compliant surcharge or cash discount program that reduces costs and boosts profitability for your business.